Profits and Profits on Exchange Rate Differences of Subsidiaries and Associated (Balance Sheet) of RUs within the same Consolidation Node must be eliminated if the RUs are consolidated at Global or Proportional Method.

The eliminated amount must be allocated on Group PROFIT and LOSS (Group and Minorities) and CONVERSION Reserve (Group and Minorities).

Set Selections

The Selections are Saved as L10-04 and Opening Select (please refer to Overview Section).

![]()

In the following steps the Eliminations happens as -(a) where a is the Conso Value cube (refer to L09) and b is the Conso Value cube (SEL L10-04).

Such amount must then be re-balanced on proper Plug Account. This happens through the "W Conso Value for L10x Elimination (total by Account)" cube that works as "bridge" cube without the Account dimension.

The Following Flow is executed :

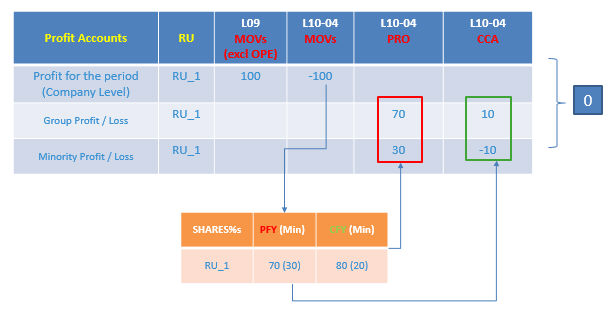

Elimination of the PROFIT Amounts at Company Level (1)

Net Profit Accounts TBs are eliminated and then rebalanced on the Group/Minorities Plug Accounts PRO Movement accoridngly to PFY Share% and CCA Movement accordingly to the Share Delta% CFY vs PFY

Attention ! Minorities calculation happens for Holding and Global Company only. Proportional Companies do not have Minorities.

Elimination of the Gain/Loss Conversion Difference Amount on RUs (2)

Exactly the same schema as above is applicable to the elimination of Profit/Loss Conversion Difference at Company Level replacing the Group/Min Profit/Loss Plug Accounts with the Group/Min Conversion Reserve Plug Accounts.

![]() The

Gain/Loss Conversion Difference is generated by the Different Exchange

Rate of the Gain/Loss Account both as Balance Sheet Account and as Revenue

- Expenses) P&L Accounts.

The

Gain/Loss Conversion Difference is generated by the Different Exchange

Rate of the Gain/Loss Account both as Balance Sheet Account and as Revenue

- Expenses) P&L Accounts.

Elimination of the Retained Earnings Amount at Company Level (3)

Exactly the same schema as above is applicable to the elimination of Retained Earning at Company Level replacing the Group/Min Profit/Loss Plug Accounts with the Group/Min Retained Earnings Plug Accounts.

In this Layer only the PAL Movement of the Retained Earning Accounts is eliminated since all the other Movements for such Accounts have been eliminated in the Net Equity Elimination Layer (L10-03).

This choice is taken to clear the Net Equity Eliminations of all the Contribution given by Exchange Rate Effects.