Investment in Subsidiaries and Associated (Balance Sheet) of RUs within the same Consolidation Node must be eliminated.

The elimination of the Investment impact the ICs Balance Sheet (the ICs play the role of controlled Legal Entities) and the RUs Profit and Loss (the RUs play the role of controlling Legal Entities)

Both impacts must be calculated highlighting the Group and Minorities contribution.

This Step executes the elimination of the TBs of those Accounts that have been tagged as Investment Elimination Y in the layer 10-02. How to setup such Account attribute please refer to Account Settings Section

Set Selections

The Selections are Saved as L10-02 and Opening Select (please refer to Overview Section).

![]()

In the following steps the Eliminations happens as -(a) where a is the Conso Value cube (refer to L09) and b is the Conso Value cube (SEL L10-02).

Such amount must then be re-balanced on proper Plug Accounts. This happens through the "W Conso Value for L10x Elimination (total by Account)" cube that works as "bridge" cube without the Account dimension.

An additional complexity is given that the balancing should be also done on the IC Balance Sheet, so the amount that has been eliminated on the RU balance sheet must be transposed on the IC balance sheet with an Xtract e re-Load process (see below).

Investment Account TBs must be differently eliminated depending from the nature of the investment. They are differently plugged depending on the nature of the Investment Cost.

- Original Cost

- re-Valuation/Depreciation

- Other

Eliminates the ORIGINAL COST of INVESTMENT (and Other) (1)

Cost is eliminated if the RU is in scope and the IC is not at Equity.

The cost is entirely eliminated .

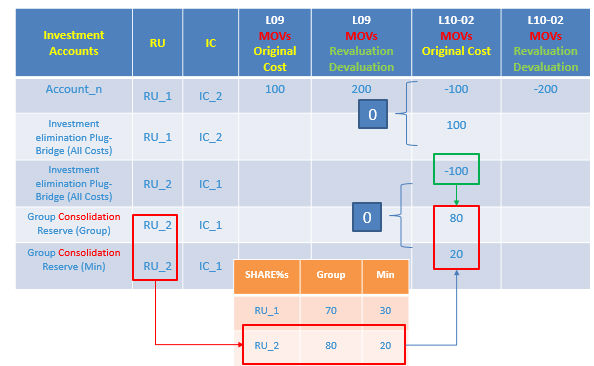

Balances Elimination on RU Plug Bridge Account (2)

The Amount that has been eliminated is re-balanced on the proper Plug Bridge Account and it is then transposed on the IC Balance Sheet.

![]()

The reversion is done extracting the Amount and re-Importing it switching the Codes between RUs and ICs.

The Plug Bridge Account has therefore no Business meaning but it is used as a Bridge to have the Eliminated Amount on the Controlled RUs (ie ICs).

Calculates the effect of Investment Elimination on ICs BALANCE SHEET (3)

The Plug Bridge Account (on IC TBs) is then re-plugged on the

> Consolidation Reserve Group and Minorities Accounts accordingly with the CFY Shares %s for all the MOVs but EDs (Exchange Rate)Movements

> Consolidation Conversion Group and Minorities Accounts accordingly with the CFY Shares %s for all the EDs (Exchange Rate) Movements

------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

Eliminates the re-VALUATION and/or de-VALUATION of INVESTMENT (4)

Cost is eliminated if the RU is in scope and the IC is not at Equity.

The cost is entirely eliminated

Calculates the effect of Investment Elimination on RUs PROFIT (P&L) (5)

The elimination of the investment impact the Profit and Loss of RUs that must be increased or decreased of the Total Amount of the re-Valuations (original cost is excluded).

The Finance Income for re-Valuation (170) is plugged with the re-Valuation (+) of Investment (Investment Cost Dimension)

The Finance Expenses for de-Valuation (180) is plugged with the de-Valuation (-) of Investment (Investment Cost Dimension),

Since the RU P&L has been changed the Profit Gain/loss at Company Level must then be recalculated

------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

Elimination of INVESTMENT in RUs @EQUITY Method (6)

The Elimination of Investment on Subsidiaries which are consolidated at EQUITY Method (Share% between 20% and 49%) has a completely different process.

The Elimination of the Investment in Subsidiaries consolidated at Equity Method is given by the difference between the Investment in Subsidiary and the pro-quota percentage of the Counterpart Net Equity.